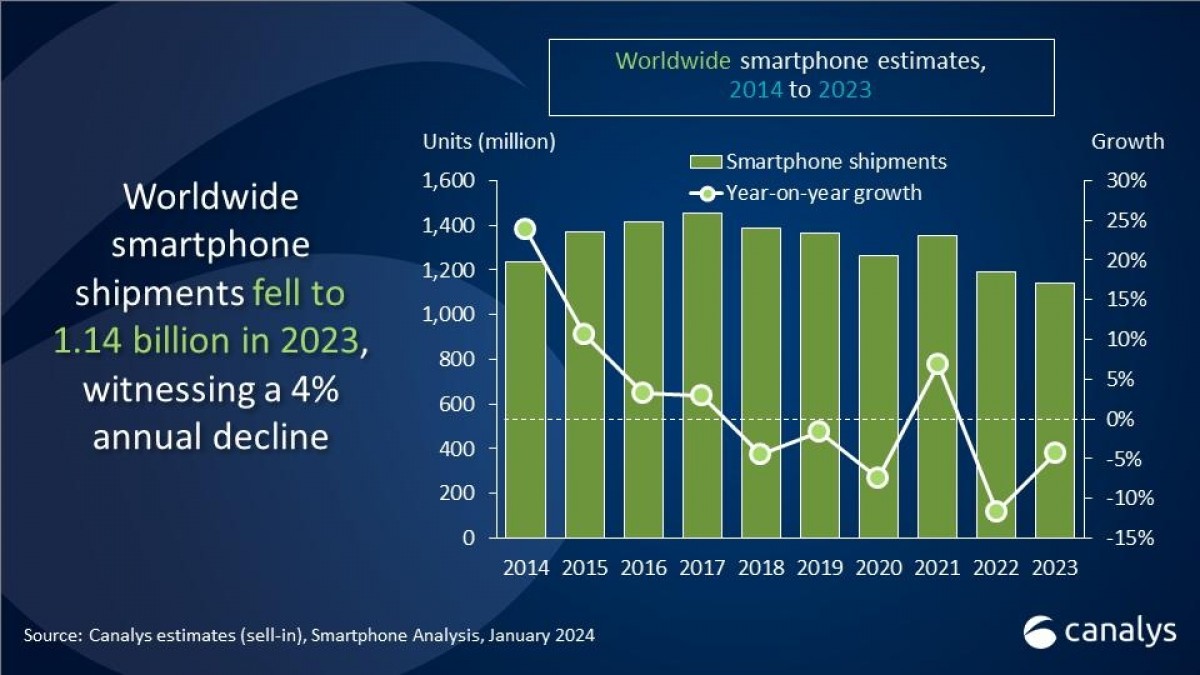

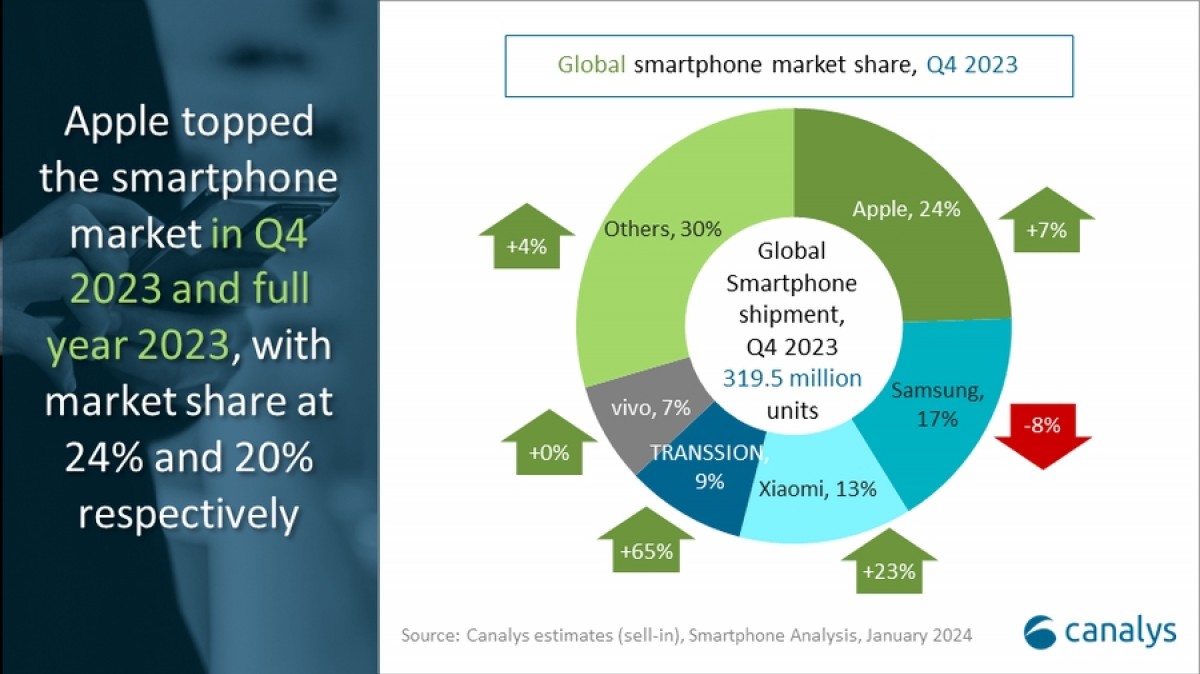

In its latest assessment of the industry, Canalys reports that smartphone shipments in 2023 came in at 1.142 billion, marking the lowest figures in over a decade. Apple secured the top position for the first time as Samsung saw a decline of 13% in a relatively stagnant year.

Analysts pointed out that the holiday season brought positive news for the smartphone market, with an 8% increase signaling a trend of stabilization.

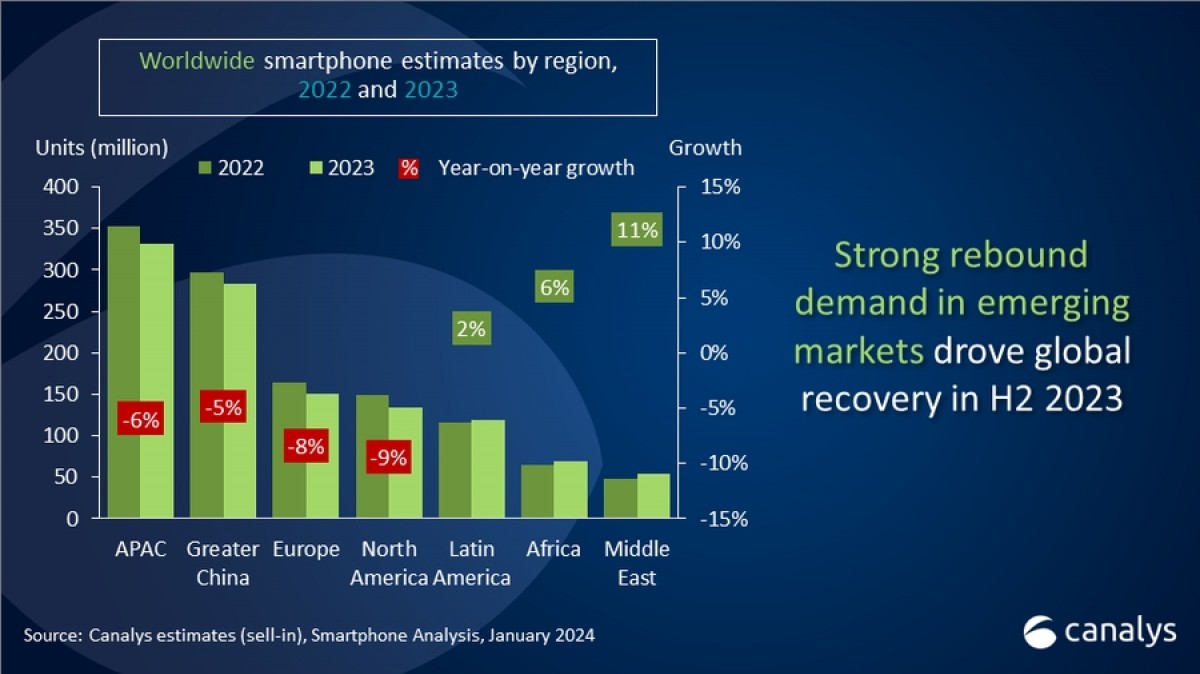

Despite significant headwinds, the smartphone market saw a recovery driven by increased demand in emerging markets, especially in Latin America, Africa, and the Middle East. These regions experienced a year-over-year growth in shipments, offsetting the declines in other parts of the world.

Transsion and Xiaomi were among the companies that benefited from the recovery, with substantial increases in shipments during the final quarter of 2023. This surge in demand propelled Transsion to fourth place for that period.

“Emerging markets will continue to be a crucial battleground for all manufacturers looking for growth, as more developed regions are experiencing reduced consumer spending and channel investments,” commented Sanyam Chaurasia, Senior Analyst at Canalys.

While the market saw a decline, the backlog of inventory is no longer a significant issue, and the affordable prices of components will allow vendors to offer more flexible incentives to consumers.

| Company | Q4 ’23 shipments (million) | Q4 ’23 Market share | Q4 ’22 shipments (million) | Q4 ’22 Market share | Change |

| Apple | 78.1 | 24% | 73.2 | 25% | 7% |

| Samsung | 53.5 | 17% | 58.3 | 20% | -8% |

| Xiaomi | 41.0 | 13% | 33.2 | 11% | 23% |

| Transsion | 28.5 | 9% | 17.3 | 6% | 65% |

| vivo | 23.9 | 7% | 23.9 | 8% | 0% |

| Others | 94.4 | 30% | 90.9 | 31% | 4% |

| Total | 319.5 | 100% | 296.9 | 100% | 8%

|

With regard to the numbers, Apple and Samsung remained the global market leaders, with Xiaomi and Oppo following in third and fourth. Companies like vivo and Honor launched flagship products and are anticipated to challenge Transsion for a spot in the Top 5.

| Company | 2023 shipments (million) | 2023 Market share | 2022 shipments (million) | 2022 Market share | Change |

| Apple | 229.2 | 20% | 232.2 | 19% | -1% |

| Samsung | 225.4 | 20% | 257.9 | 22% | -13% |

| Xiaomi | 146.4 | 13% | 152.7 | 13% | -4% |

| Oppo | 100.7 | 9% | 113.4 | 10% | -11% |

| Transsion | 92.6 | 8% | 73.1 | 6% | 27% |

| Others | 347.9 | 30% | 364.1 | 31% | -4% |

| Total | 1142.1 | 100% | 296.9 | 100% | -4%

|

In the coming year, manufacturers are expected to take two strategic directions – investing in on-device AI or expanding shipments in the mid-to-low-end segment. While Samsung launched its Galaxy S24 smartphones featuring Galaxy AI globally, Chinese companies introduced these phones in the domestic market, indicating the intention to expand internationally.

Mass-market products will be the focus for vendors, with affordability and value-for-money proposition as core product strategies in the short term.